Table of Content

By saving even a little bit on a consistent basis, your money can grow substantially over time. This calculator helps you estimate the earnings potential of your contributions, based on the amount you invest and the expected rate of annual return. That already sounds attractive, but some taxpayers are eligible to supersize their contributions and save even more — if their employers allow after-tax contributions to their 401. These plans allow you to contribute up to $37,000 more than the $19,000 limit. This means you can potentially save $56,000 annually in an after-tax 401 (that’s up to $62,000 if you are 50 or older).

Your circumstances are unique; therefore, you need to assess your own situation and consult an investment professional if you feel you need more personal advice. Also, you should remember that the results you receive from this calculator do not account for tax effects of any kind. Therefore, the dollar amount of your actual plan contribution may be less than the estimate provided by the calculator. In addition, your circumstances will probably change over time, so review your financial strategy periodically to be sure it continues to fit your situation.

Current Age

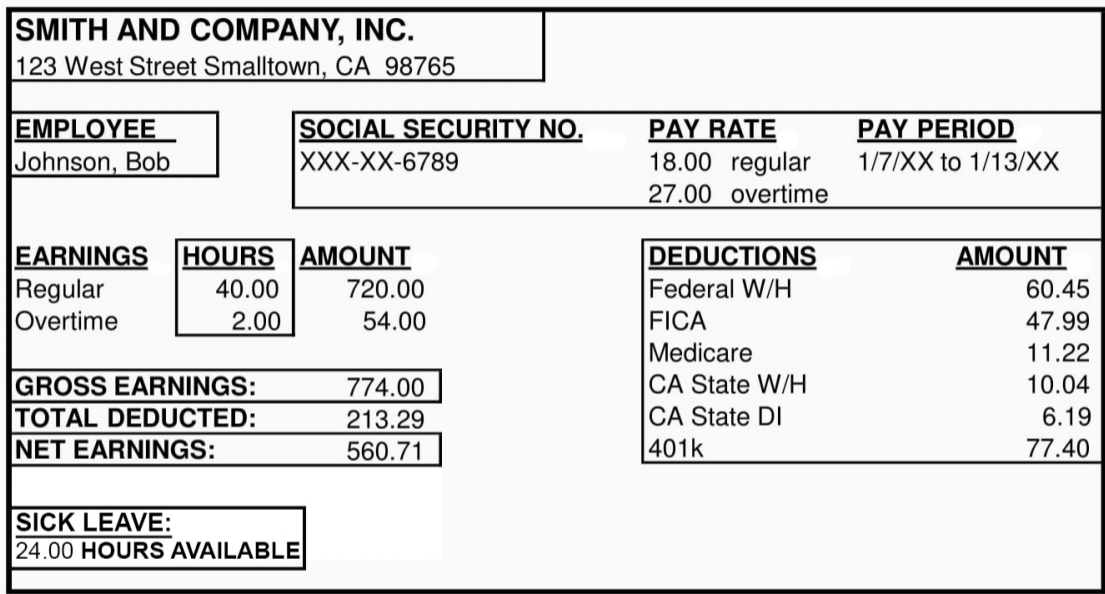

Your 6% of $30,000 will amount to $1,800 per year, and the company match will be an additional $1,050, for a total contribution of $2,850. We won’t go into all of the details behind a W4 at this point, but for the sake of the example, we’ll say you filed your W4 to exactly match your tax expected of $1,970 for the year . In addition to this, you have opted to take advantage of your employer’s health insurance plan, which costs $50 per month. You are paid on an every-other-week schedule, for 26 pay periods per year. With so many payroll deductions, it is common for many people to feel their take-home pay is almost gone by the time it gets to them.

Enhanced safe harbor plans match 100% of employee contributions up to 4% of compensation. Try entering different percentages until you land on a figure you can live with for both today’s and tomorrow’s needs. Your ability to save may fluctuate in different stages of your career, so revisit this calculator periodically.

Paycheck impact calculator

You do have to pay tax on withdrawal, however, at which point the money is taxed as income. Nevertheless, contributing to a traditional 401 will greatly reduce how much income tax you pay in your lifetime. The portion of your paycheck that you should contribute to your 401 depends on your age, your company policy, and your general financial situation. The younger you are when you start a 401, the less you might need to contribute from each paycheck.

Step #4 – Divide the interest rate by the number of periods the interest or the 401 Contribution income is paid. For example, if the rate paid is 9% and compounds annually, the interest rate would be 9%/1, which is 9.00%. Step #3 – Now, determine the duration left from the current age until retirement. Step #1 – Determine the initial balance of the account, if any.

Federal 401k Calculator

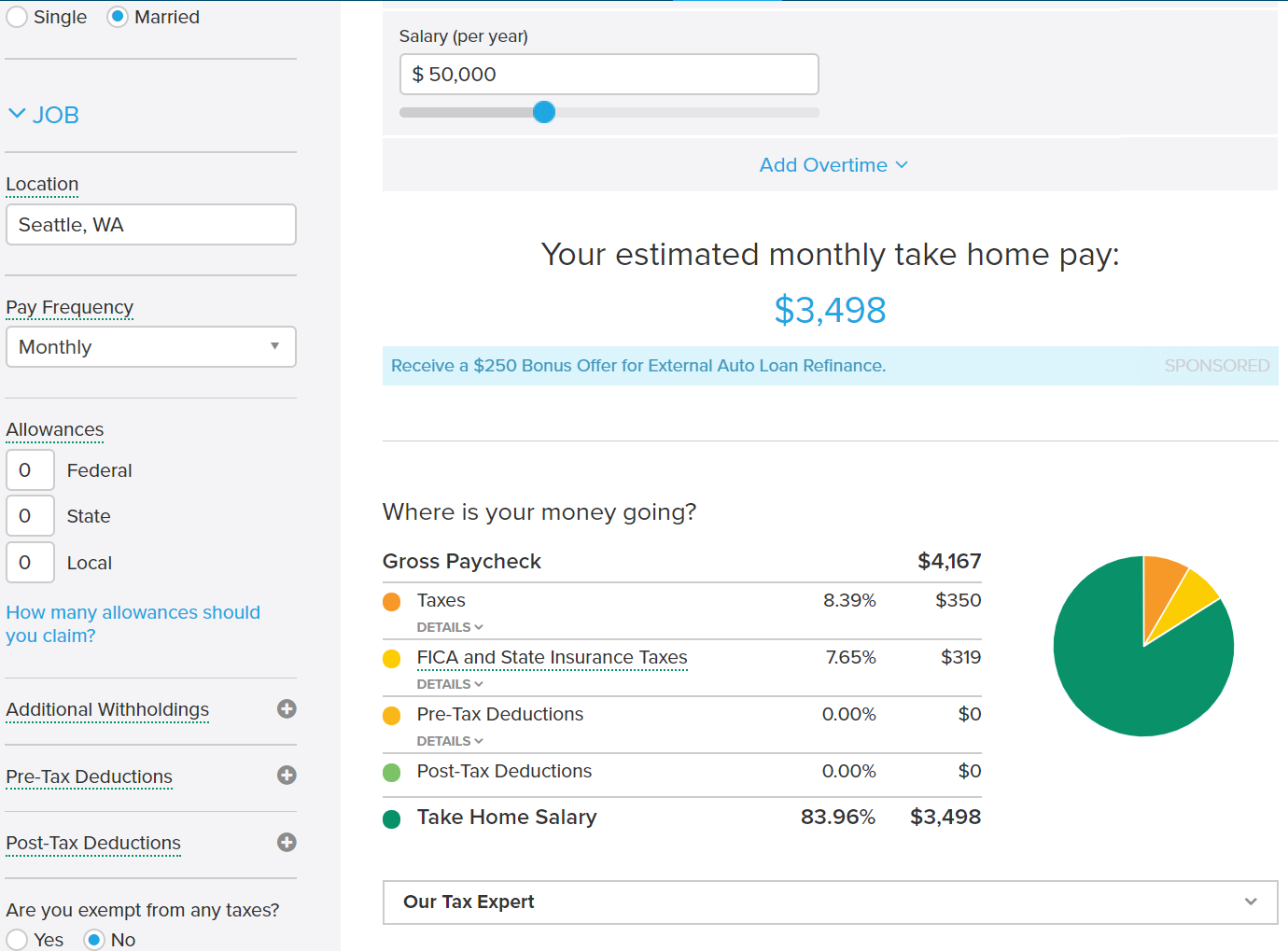

Talk to a financial advisor who can take you through the steps and help you set up an account if you're at all uncertain about how to start investing for retirement on your own. This article is reprinted by permission from NerdWallet.The investing information provided on this page is for educational purposes only. NerdWallet does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments. The impact of your contributions and tax savings on your take home pay. As you can see, going with the ‘wait until next year’ strategy can have a significant effect on future savings. Retirement comes faster than you think, and by not starting a plan now, you and your employees are missing out on compound interest.

A Roth 401 is similar to a Roth IRA in that your contributions won't reduce the amount you pay in taxes each year. But the benefit of not paying taxes on your earnings can pay off when you reach retirement age. Contributing to an employer-sponsored retirement plan, like a 401, allows you to save for retirement — and get a tax break for doing so.

About 401(k) Contribution Calculator

And an inflated income can have a ripple effect on a few other things, like your general tax liability. If you’re retired or about to retire, it can also affect how much of your Social Security is taxable and how much you pay for certain Medicare premiums. Roth IRA conversionsallow you to transfer the assets in your traditional IRA into a Roth IRA so that your investments’ growth, and qualified withdrawals, get tax-free treatment in the future.

ADP offers a set of helpful calculators and tools to engage your workforce and help them with important financial decisions. See how we help organizations like yours with a wider range of payroll and HR options than any other provider. Explore our full range of payroll and HR services, products, integrations and apps for businesses of all sizes and industries. Retirement Specialists provide information for educational purposes only. Retirement Specialists are Registered Representatives of Nationwide Investment Services Corporation, member FINRA, Columbus, Ohio.

©2022 Standard & Poor’s Financial Services LLC. The S&P 500® Index is composed of 500 selected common stocks most of which are listed on the New York Stock Exchange. This calculator uses the latest withholding schedules, rules and rates . More aggressive and riskier investments can help you earn more if you're still young. But you should move to more conservative investments that are safer as you get older. You might not have enough time for the economy to recover if it goes through a slump. Real-time last sale data for U.S. stock quotes reflect trades reported through Nasdaq only.

Further, the employer contribution will also be calculated subject to limits decided by the individual’s employer. But there are several benefits to establishing a plan, including that contributions you make can lower your taxable income. Contributing to an employer-sponsored 401 retirement plan can be a great way to save money toward your long-term financial goals. That's because of the interaction between contributions you make and how much money is withheld through Form W-4. Let's look more closely at how these two tax topics relate to each other and what you can do to account for both properly. The advantage of traditional 401 plans is that you contribute with pre-tax dollars.

Let's see how to rebalance those assets back to their target allocations. With the GuidedSavings tool by GuidedChoice®, you'll receive a detailed and personal analysis of all of your retirement factors. This analysis will provide a specific recommendation that you can follow, or you may decide to implement a strategy of your own. Enter what you have currently saved, how much you could put in a monthly contribution to a 401, and how much your employer/the business owner may match. Begin with information about you, including your annual salary, the state you reside in, your current age, and the age you aim to retire. Enter up to six different hourly rates to estimate after-tax wages for hourly employees.

The market will go up and down, but you should be in a more comfortable position when it comes to retiring if you continue to invest. The sacrifices you make now by contributing to retirement will prevent you from having to make more difficult decisions when you're retired. Default is 0% based on the assumption that salary increases will be nullified by inflation.

But your pay might not be greatly reduced when you increase the amount you contribute each month. One of the easiest ways to increase the amount you contribute is to add to the amount each time you're given a raise. You might not even notice a difference in your take-home pay in this case. Because the more you contribute by Dec. 31, the more you can shave off your taxable income for the year. Your earnings are based on the market return percentage you provided. Earnings are calculated annually and include each year's total contributions.

Sometimes, these plans are offered through third parties, and they may have high fees and investment portfolios not performing to your satisfaction. In addition, you have additional vehicles to invest in outside your workplace, like Individual Retirement Accounts and Roth IRAs, among others. When you contribute to a 401, your taxable income goes down, and so the amount of tax that your employer calculates to have withheld from your paycheck also goes down. Therefore, your take-home pay will fall by a smaller amount that you have contributed to your 401. When you choose to participate in your 401 plan at work, you divert part of the money that would ordinarily go into your paycheck and instead have it put into your retirement plan account. Therefore, it's natural to expect that your take-home pay will drop by the amount you divert into the 401.

No comments:

Post a Comment